The Supplementary Appropriation Bill: Some comments

By R. Chand

It will be foolhardy to read much into this universal acclaim for the building up of this rainy fund, a recent addition to the Special Funds, has had a cost. The 2011 Public Expenditure and Financial Accountability (PEFA) Assessment report noted that “One of the interesting features of the Mauritian budget over recent years has been the government’s response to the underspending on the capital side.

Rather than allowing the underspends to flow through to the budget bottom line, resulting in smaller deficits, the government has reappropriated the funds, and transferred them to a set of Special Funds, which can subsequently spend the money on specific items over a period years.”

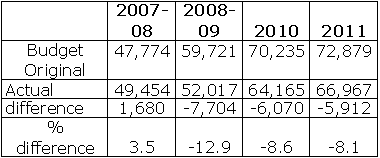

This transfer of funds to Special Funds is some sort of colourable accounting not in accordance with the GFSM 2001 standards. Actually they should be treated as below the line financing items. Over Rs 15 billion or 4.2 percent of 2012 GDP have been transferred to these Funds. These Surplus Funds were unspent at the year-end. The use of Special Funds to transfer spending from one year to the next, and from one function to another outside of the Budget creates uncertainty, and undermines the credibility of the Budget. Indeed, as shown in Table I the difference between actual primary expenditure and the originally budgeted primary expenditure (i.e., excluding debt service charges) has consistently been high since 2008.

Table I: Government Primary Budget & Actual Expenditure

after adjusting for transfers to Special Funds

What Moody seems to have missed out was that it was the chronic underspending in capital projects that created the unequalled but unutilised Special Funds. The underperformance in capital expenditure meant a low implementation capacity for many of the projects announced in the Budget. Fiscal adjustment relied mainly on lower capital expenditures at a time when the economy sorely needed to bridge the infrastructure deficit. The economy continues to be constrained by skills mismatch, supply-chains bottlenecks — efficiency in port, airport, road congestion, cost of energy and telecommunications — the need for diversification of markets and products and lack of innovation and enterprise. The average capital expenditure over the period 2006-11 (2.6%) fell short of that of period 2000-05 (4.1%) by around 1.5% of GDP annually. This amounted to around Rs 21 billion of investment that were foregone over five years.

The ability to implement capital projects has picked up recently with the Project Monitoring Unit at the PMO which is addressing some of the capacity constraints within the public service and across sectors. As at May 2012, though on a purely cash basis, Government has spent less than Rs 2.7 billion on out of a capital budget of Rs 14 billions, which amounts to only 19 % of the earmarked capital expenditure.

Table II : Capital expenditure as a % of GDP

There were also large variations between announced and actual programme expenditure. Only for goods and services additional expenditures were on average more than 100% above voted expenditures and on a purely programme basis it was above 200%. Such variations adversely affect the allocative efficiency of the Budget.

Perhaps this was what motivated Mr K. Li Kwong Wing to question the Programme-Based Budgeting (PBB): “Do we get value for money? Is there quality control? What is the cost effectiveness of all these excess expenditures we are called to approve? Are we making proper use of the management tool of Programme-Based Budgeting and the Performance Management System which supposedly has been installed at the Ministry of Finance by experts from the World Bank? What’s the use of all these advisers from the World Bank and consultants posted at the Ministry of Finance if there is no monitoring, no control, no evaluation to meet these key performance indicators and targets?”

These comments, we hope, will provide welcome visibility to an important topic like PBB whose implementation has totally been bungled.

Besides the substantial contingency funds provided in the budget process, which are effectively unallocated during the budget process and then distributed as the year progresses, some of the variations may be explained by the lack of proper linkages between the macroeconomic projections, fiscal strategy and ministry level strategic plans. Moreover, as pointed out by the PEFA Report, the ministries and departments are not provided enough time to prepare meaningful budget submissions — “… the quality of some of the submissions related to capital projects is inadequate as a result of the need to meet budget deadlines… The setting of expenditure ceilings for the budget circular however, receives limited policy inputs from budgetary bodies, leading to relatively weak policy rationales behind the ceilings, and weak acceptance of the ceilings by ministry policy makers.”

Arguing that “Government has created the funds in case we need money like any prudent man would do” is not sound economic logic. The availability of funds would not have been a problem even without a Moody’s upgrade of our Baa2 rating. It is beyond understanding that the fiscal space generated over the past four budgets were allowed to lie lamely in bank accounts; we were marking time and keep missing out targets while there were so much to catch up in terms of infrastructure priorities.

It would have been more logical to show lower budget deficits and borrow from the market whenever there was a need for additional funds for the implementation of capital projects. What’s more mind-boggling and scandalous was that over the past five years some Rs 45 billion of external borrowings (out of which only Rs 5 billion were utilised) were contracted sometimes at unreasonable above-average market rates. Thus the universal acclaim for the shifty tricks of parking Special Funds outside the budget in idle bank accounts to hide the ineffectiveness in implementing capital projects did miss out on its serious economic consequences.

In pure economics terms, it means an opportunity cost of billions of rupees of projects foregone over five years reflecting the inability of the Ministry of Finance to do anything beyond its core mission of fiscal-deficit reduction at any cost — be it at the cost of structural reforms or productivity-enhancing capital expenditures.

* Published in print edition on 3 August 2012

An Appeal

Dear Reader

65 years ago Mauritius Times was founded with a resolve to fight for justice and fairness and the advancement of the public good. It has never deviated from this principle no matter how daunting the challenges and how costly the price it has had to pay at different times of our history.

With print journalism struggling to keep afloat due to falling advertising revenues and the wide availability of free sources of information, it is crucially important for the Mauritius Times to survive and prosper. We can only continue doing it with the support of our readers.

The best way you can support our efforts is to take a subscription or by making a recurring donation through a Standing Order to our non-profit Foundation.

Thank you.