M. Kanhaya

Competitiveness not an option anymore !!!

— M. KANHAYA

A proper assessment of our external competitiveness with respect to our major trading partners by examining a variety of indicators will shed some light over some of the present policy implications of dealing with an appreciating rupee. What is meant by the competitiveness of an economy?The concepts of competitiveness are the short-run versus long-run view of competitiveness and price versus non-price measures of competitiveness. The commonly used measures of competitiveness are multilateral or nominal effective exchange rate (NEER), real exchange rates and real effective exchange rate (REER). In the long run, competitiveness reflects the ability of an economy to improve living standards. In the short-run, the focus is on the current account-price competitiveness. The REER is an indicator of competitiveness. An assessment of external competitiveness should examine exchange rate developments, price developments, cost developments, productivity and unit labour costs (ULC).

Among the variety of alternative indicators of external price competitiveness, the principal among these is the real effective exchange rate, which measures the price of domestic goods and services in terms of foreign goods and services. First of all, let us define the Nominal effective exchange rate (NEER). The NEER takes into account the fact that we have several trading partners. Conceptually, the NEER attempts to capture what an exporter effectively receives in local currency for one unit of exports. How is this measured? The Nominal Effective Exchange Rate (expressed as an index) is the ratio of an index of a currency’s average exchange rate to a weighted geometric average of exchange rates for the currencies of selected countries and the euro area.

The NEER is a nominal variable. The Real Effective Exchange Rate (REER) is a nominal effective exchange rate adjusted for relative movements in national price or cost indicators of the home country and selected other countries. An increase in the REER rate means that the relative price of a country’s goods increases. This could be the result of increases in wages and prices, assuming that the nominal exchange rate remains the same. Such an increase is not good for the export sector. Either producers will find it more difficult to sell goods abroad at the higher price, or they will have to absorb the higher cost of production by reducing profit margins. In either case, production in the export sector is likely to suffer, and so will employment. Changes in REER can be interpreted as reflecting changes in competitiveness of an economy. The REER increases when one of the following happens: domestic prices increase, the NEER falls, or the world market price falls. Thus the real effective exchange rate measures the competitiveness of a country with respect to its main trading partners.

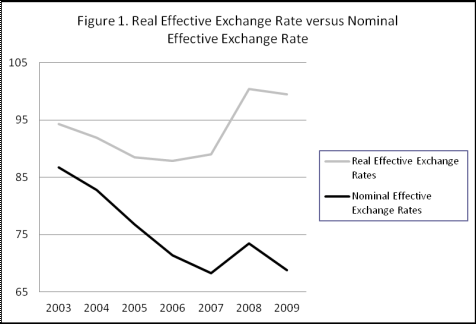

The graph below shows that the rupee has appreciated substantially in real effective terms since 2006. Mauritius’ real effective exchange rate has appreciated by around 13% over the past four years. This loss of external price competitiveness was not driven almost entirely by nominal effective exchange rate for the latter depreciated by some 3% over the period. Even if the authorities are able to prevent nominal exchange rate appreciation, real appreciation occurred through relatively higher domestic inflation. The divergences of the real effective exchange rate from the nominal effective exchange rate reflect the accumulated inflation rate differentials relative to trading partners.

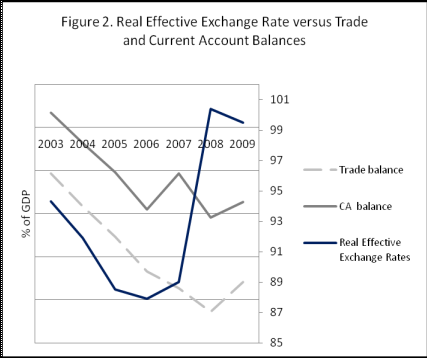

In the absence of offsetting factors, this broadly based loss of external price competitiveness will raise the trade and current account deficits, draining official foreign exchange reserves. The appreciation in the real effective exchange rates contributed to the trade and current account imbalances. The real effective exchange rate is plotted versus its trade and current account balances in Figure 2. The trade deficit has tended to increase when the rupee has appreciated in real effective terms, raising the current account deficit. This co-movement between the trade deficit and the real effective exchange rate is strengthened by abstracting the irregular items in exports and imports as from 2007.

Competitiveness is an imperative not an option in today’s global economy

Comparing the changes in unit labour costs (ULC) in the manufacturing sector with other countries, we notice that most of them were experiencing a relatively lower increase in ULC, the steepest growth being for Mauritius (10.0%). The ULC in dollar terms increased by around 21.7%, one of the highest, explained by the high appreciation of the rupee relative to the US Dollar. We certainly have lots of catching up to do in the productivity race. Until we catch up, some may recommend there may be little choice than to achieve external competitiveness by allowing the rupee to depreciate.

Table 1 — Manufacturing Unit Labour Costs of selected countries, 2008

Before we deal with the depreciation issue, we should examine some of the factors that explain this appreciation of REER. Normally, when a country runs a moderately high current account deficit and the relatively rapid inflation which averaged 7.5% over the past four years is weakening its competitiveness, one expects to see a depreciation of its currency to bring about an adjustment in imbalances. The opposite seems to have happened. What’s more, this pattern has persisted up to now, with the REER continuing to appreciate. But as long as we have the large capital inflows and the Central bank adopts a non-interventionist stance towards the currency market (and part of the positive huge net errors and omissions exceeding Rs10-13 billion) and if capital inflows stay robust, there will be a continuing upward pressure on the REER. In such a situation depreciation of the rupee is a purely temporary solution which is not sustainable.

In particular, large capital inflows that do not boost export potential in the short term could lead to an increase in real wages and real exchange rate appreciation, and a fall in the marginal product of investment. Thus, in situations where domestic savings are insufficient, the use of foreign capital to finance investment may further depress the profitability of investment by causing the exchange rate to be overvalued – a form of what is commonly known as “Dutch Disease”. The consequences of these capital inflows on the competitiveness of the real exchange rate may then be an important contributory factor to the patterns we observe — the country becoming increasingly uncompetitive on the trade front.

So what should be the design of policy responses in the face of the large capital inflows and what is the effect of policy responses on the behaviour of the real effective exchange rate? In the recent IMF paper “Capital Inflows and Balance of Payments Pressures — Tailoring Policy Responses in Emerging Market Economies (EMEs)” relating to cases of countries that have a current account deficit and where the net total capital flows substantially exceed this deficit, their recommended policy response is (a) to allow limited nominal exchange rate appreciation (whereas a large appreciation, by making investment in the country more expensive, would deter further inflows); (b) do not sterilize reserves accumulation for it will hike up interest rates that will encourage continued capital inflows; (c) do not tighten monetary policy because the resulting higher interest rates are likely to exacerbate the capital inflow problem; (d) tighten fiscal policy, especially if there are inflationary pressures; this will lower interest rates and reduce capital inflows; and (e) relax controls on capital outflows and possibly impose controls on inflows. In the immediate, a combination of sterilised currency intervention and capital account management may be unavoidable to prevent further rupee appreciation.

As some countries’ exports are getting affected, some governments are taking several steps to neutralize the effect of currency appreciation. Losses due to currency appreciation are partly being neutralized with lower cost of production emerging from higher productivity( equity participation, restructuring and improvements in management, technology upgrading and product rationalisation and general cost-cutting).

Within the industrial sector also, the effect of rupee appreciation varies among firms. More productive firms can absorb the loss in a better way. Also, due to volatile currency market, firms are being encouraged to adopt sophisticated methods of risk management. Exporters are being told to use forward contract to switch the invoice currency into strong currencies by paying nominal charges without bothering the foreign buyer to change the invoice currency.

In some sunset sectors, we cannot continue with business as usual; we may have to consider some closures and retrenchment of workers. We should envisage tapping fully the Empowerment Programme for retaining and reskilling to redirect recycled workers to other more promising sectors. We will have to constitute a permanent think-thank/Unit to accelerate the diversification of the economy — what the new-socio economic model had failed to deliver.

M. KANHAYA

An Appeal

Dear Reader

65 years ago Mauritius Times was founded with a resolve to fight for justice and fairness and the advancement of the public good. It has never deviated from this principle no matter how daunting the challenges and how costly the price it has had to pay at different times of our history.

With print journalism struggling to keep afloat due to falling advertising revenues and the wide availability of free sources of information, it is crucially important for the Mauritius Times to survive and prosper. We can only continue doing it with the support of our readers.

The best way you can support our efforts is to take a subscription or by making a recurring donation through a Standing Order to our non-profit Foundation.

Thank you.