The 29th MPC: Growth first !!!

By R. Chand

While no one underestimates the need to fight inflation or to have a lower debt-to-GDP ratio, one still needs to ask if our two major institutions, the MOF (on the fiscal side) and the BOM (on the monetary side) are not sidelining the growth factor in a global environment where Mauritius should be having higher investments, creating more jobs and growing faster…

From the minutes of the 29th Monetary Policy Committee (MPC) Meeting of the 11 March 2013, it seems that both the Ministry of Finance (MOF) and the Bank of Mauritius (BOM) are not focussing on the issues that really matter. The fiscal policy/monetary policy regime influences the depth and duration of downturns and time for recovery. With economic growth clocked at an average annual rate of 3.5% for the past five years, is it not time to review the country’s growth strategies? Growth must come up first!!! To the Governor of the Reserve Bank of India, Dr D. Subbarao’s concern that a Central Bank must be responsive to the needs of the downtrodden (in its pursuit to rein in inflation), there is also the argument that growth is the right potion to lift the poor out of poverty, be it directly through government programmes or indirectly through a trickle-down strategy. But how long will the general public accept low growth and its manifold negative impacts on them?

While no one underestimates the need to fight inflation or to have a lower debt-to-GDP ratio, one still needs to ask if our two major institutions, the MOF (on the fiscal side) and the BOM (on the monetary side) are not sidelining the growth factor in a global environment where Mauritius should be having higher investments, creating more jobs and growing faster.

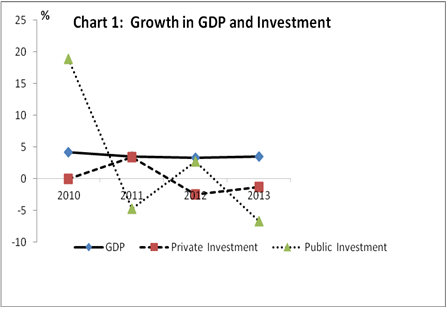

The revival of growth from its current level of 3.5% to its potential of about 5 to 6% depends on a higher rate of investment in the economy. It is now more than four years since private investment peaked at 21% of GDP before falling to the current level of 17%. Public Investment as a percentage of GDP is expected to be as low as 5.1% in 2013 from a high of 6.6% in 2009. Both public and private sector investment (exclusive of aircrafts) are expected to contract in 2013 — public sector investment declining by 6.7% and private sector investment by 1.3%. (See: Chart 1)

A narrow fiscal policy stance: The foremost challenge for returning the economy to a high growth trajectory is to boost capital spending. This is the remit of fiscal policy; it is not a monetary policy problem. In the present sluggish growth environment, fiscal policies in several countries are providing a massive stimulus to aggregate demand especially through higher capital spending. When the volume of investments increases, the potential for further investment expands and this eventually raises the economy’s capacity for growth.

The MOF appears to be holding the economy down with its mix of rigid control of the level of public debt and its reluctance to boost capital expenditure, i.e., public sector investment. In his presentation to the MPC, the Financial Secretary, Mr Ali Mansoor, posited that there was little room left for fiscal policy to further support the expansion of the economy and admitted therefore the inability of the MOF to overcome the implementation capacity constraints. Fiscal policy, he added, was expected to end up neutral or even contractionary in 2013 because of the need to control the total amount of government debt.

With a budget deficit targeted at 2.2% of GDP for 2013 and some Rs 10 billion lying idle in Special Funds, we believe that there is more than enough resources for an expansionary fiscal policy. The lack of fiscal space is not a solid argument. As RBI Governor Dr Duvvuri Subbarao rightly put it in his IG Patel Memorial Lecture at the London School of Economics on 13 March 2013: “Growth slowdown can be mitigated, indeed growth can be aided, provided attention is paid, along with the quantum of fiscal adjustment, also to its quality. Experience demonstrates that even if total expenditure as a proportion of GDP is curtailed, it need not dampen growth; on the contrary, if there is switching from current expenditure to capital expenditure, fiscal consolidation can actually stimulate growth by ‘crowding in’ private investment.” But here also the MOF fails to re-order its expenditure plan in favour of more targeted expenditures that help build diversified productive capacity for the future.

As for the level of debt, it is not as simple as it is being presented by MOF. Whether it is presently a problem depends on how far the economy is from its productive capacity, where future deficits are likely to grow or shrink as the economy moves towards full capacity and the likely effect of taxes and spending on growth of that productive capacity in the long term. Good fiscal policy can enhance the global competitiveness of the economy and unleash substantial growth. If we get higher growth, tax revenues will increase as well the ability to pay down debt. That’s why we need good policy right now, which can only be arrived at through thoughtful debate and compromise.

The question of how we induce enough investment to build the production capacity required in the years ahead necessitates a vigorous debate. But dogmatic responses to budget deficits are not conducive to this sort of examination. Too much of fiscal rigour appears to be weakening the economy, not strengthening it. The MOF cannot kick responsibility down the road; it is its responsibility to generate medium- to long-term structural reforms and capital spending to enhance productivity and competitiveness to keep the growth engine running and lift sluggish growth.

What is really at issue is not the lack of fiscal space or the limit to our ability to absorb more borrowing. It is too much focus on the size of the Budget rather than on the quantum of creative new policy thinking; it is the latter that matters more-New thinking and policies that could have generated stronger fiscal management, higher quality public spending and long-term investment programs for infrastructure, for renewable energy, mass transit system, innovation, large-scale skill and job training, and so forth. These require thinking and planning of the kind that has never happened with the MOF’s short-termism and its overly budgetary focus. Despite its Programme Based Budgeting, which has remained a mere theoretical tool failing to bring efficiency gains, and its Public Sector Investment Programme (PSIP), which is a mere wish-list of projects rather than a well-planned prioritised list of much-needed infrastructure projects, the MOF is finally admitting that it has not been able over the years to address the implementation capacity constraints within the public service and across sectors.

The glaring instances of inadequacies in concept, design, execution and monitoring of projects, cost overruns, unforeseen delays and the technical and legal proceedings that have far-reaching effects on projects have continued year after year to adversely affect the implementation of capital/infrastructure projects. The MOF did not give the more powerful growth impulses to the economy because the burden of fiscal consolidation fell mainly on capital expenditures — a failure to ensure the “deliverology” on our priority capital projects. The country needs productive public investments, not wasteful spending to rev up growth. The final test for fiscal policy as a development tool is its ability to deliver results. It is time the Ministry of Finance moved out of the fiscal straightjacket and started looking beyond sticking to “good” statistics. The situation demands that policy-making should transcend present conceptual limitations and go for targeting substantive higher growth.

A Conservative Monetary Policy Stance: In the light of moderate inflation (2.9% in January and 3.6% in March) and decelerating GDP growth, we expected the BOM’s monetary policy stance shifting to support growth, taking a cue from the Federal Reserve’s aggressive easing of monetary policy which is proving surprisingly effective at blunting the blow to the economy from tighter fiscal policy. Many economists have been scrambling to raise their growth forecasts. And in India, the RBI cut its benchmark policy rate by 25 basis points, for the second time since the start of the year, in a bid to help revive flagging growth.

What is surprising is that the MPC’s outlook remains hawkish; it sees upside risks to inflation despite acknowledging that the threats to the growth outlook outweighed inflation worries and, more importantly, accepting that monetary policy could not insulate the public from an increase in the cost of living and decrease in real income if they originated from an exogenous rise in world oil or food prices or other deterioration in the country’s terms of trade.

On the basis of these arguments, we believe that there is need to revisit the ideal inflation target, as carried out in India which that led to a lowering of its repo rate to support the economy. Our inflation target may be too low for the current environment. That target may be more relevant for the period before the crisis began afflicting the global economy about four years ago. An inflation target that is nearer to our historical rate will give more elbowroom to the BOM to lend some support to the economy.

We believe that the MPC’s stance should have been more growth supportive. As pointed out by J. Stiglitz in the 15th C. D. Deshmukh Memorial Lecture on “A Revolution in Monetary Policy: Lessons in the Wake of the Global Financial Crisis” on 2 January 2013 in Mumbai: “The crisis has forced many Central Banks to rethink their doctrinaire policies (…) monetary and fiscal policy needs to be coordinated, and it makes no sense for the body controlling one of these to be allegedly independent, while the one responsible for the other is politically accountable (…) Central banks should broaden their objectives beyond inflation. They need to focus too on employment, growth, and financial stability. And monetary policies need to be coordinated with fiscal policies.”

* Published in print edition on 30 March 2013

An Appeal

Dear Reader

65 years ago Mauritius Times was founded with a resolve to fight for justice and fairness and the advancement of the public good. It has never deviated from this principle no matter how daunting the challenges and how costly the price it has had to pay at different times of our history.

With print journalism struggling to keep afloat due to falling advertising revenues and the wide availability of free sources of information, it is crucially important for the Mauritius Times to survive and prosper. We can only continue doing it with the support of our readers.

The best way you can support our efforts is to take a subscription or by making a recurring donation through a Standing Order to our non-profit Foundation.

Thank you.