The 2019/20 Budget: Beyond Reasonable Limits

By Sushil Khushiram

The 2019/20 Budget is aptly summed up by the plethora of mini-measures to provide tax sops and monetary transfers to the population at large, in almost every category and capacity. Its populist slant, designed to attract political support for the incumbent Government in view of the forthcoming elections, is a fitting apotheosis to the generous social spending policies pursued in several successive budgets since 2015.

Oversize Deficits

That a Government should engage is some additional public spending to follow the electoral cycle is not a novel phenomenon. But with the accumulation of high successive deficits, the build-up in public debt has now grown to unprecedented levels. The annual trend in the main budgetary aggregates as from 2014 is shown in Table 1. The fiscal deficit for 2019/20 is budgeted at 3.2% of GDP, but is actually much higher at 5.8% of GDP, after consolidation with special funds and including off-budget expenditures, as explained in Box – Masters of Deception (1.1).

Assuming the usual undershooting in capital spending, the revised 2019/20 deficit is estimated at 5% of GDP, only slightly higher than the figure of 4.8% of GDP recorded in the previous fiscal year. The evolution of the fiscal deficit is explained in Box 2. Current expenses have grown by over 3 percentage points from 2014 to 24.6% of GDP, while total expenditure will be close to 28% of GDP in 2019/20.

A comparison of budget aggregates between two consecutive five-year periods, namely, between 2010 to 2014, and 2015/16 to 2019/20, as shown in Table 2, reveals that the average budget deficit in the more recent period worsened moderately, and that revenue, current expenses, and total expenditure grew faster on average. Current expenses grew almost twice as fast, or by an average of 9.3 % annually. However, the average annual growth in capital spending was lower, leading to a drop in its average share of GDP from 3.6% to an estimated 2.4%.

The expansion of social welfare spending has been largely at the expense of building capital infrastructure, despite the more recent implementation of the large Metro Express and Cote d’Or Multisports projects. Social benefits have increased from Rs19 bn in 2014 to Rs34 bn in 2019/20, overtaking compensation of employees as the largest component of current expenses. These two items now account for about half of total current expenses.

Elevated Public Debt

Public Sector Debt (PSD) has been rising steadily over time to over 65% of GDP, which is the statutory ceiling set for any fiscal year end under the Public Debt Management Act (PDMA). Public sector debt is officially estimated at Rs322.6 bn, or at exactly 65% of GDP at end June 2019. However, the official figure underestimates PSD by a concocted adjustment item of Rs4 bn, as explained in Box – Masters of Deception (1.2). Excluding this amount from public debt, PSD totals Rs326.6 bn, or 65.8% of GDP at June 2019, exceeding the PDMA debt ceiling.

1. The operating deficit started to worsen from 2015/16, as current expenses expanded more rapidly than revenue.

2. Capital expenditures were cut sharply in 2015/16, and remained depressed in the following two years, to contain the impact of fast-rising current expenses on the overall deficit.3

3.In this fiscal year and the next, current expenses continue to increase, but the operating deficit is stabilized with the help of foreign grants, mainly from India.

4.However, a recovery in capital spending, mainly from off-budget expenditures for Metro Express and the Multisports Complex, is causing further deterioration in the overall budget deficit.

5.The financing of successive sizeable deficits is leading to an elevated level of public debt, which is not sustainable in the longer term, in view of the growing weaknesses of the Mauritian economy, and of mounting global financial risks.

Government-guaranteed borrowings through foreign lines of credit are accounted for in PSD only to the extent that the credits are disbursed. For greater fiscal transparency, PSD should be calculated to reflect both debt disbursements and debt commitments. The India Eximbank line of credit of US500 mn to the State Bank of Mauritius, mainly for Metro Express, would add 3.6% to PSD to reach 69.4% of GDP. Counting the committed value of the China Eximbank credit to Mauritius Telecom for the Safe City Project, and other possible contingent liabilities, PSD at June 2019 well exceeds 70% of GDP.

The latest IMF Report on Mauritius draws attention to “public debt statistics that do not factor in borrowing outside of the central Government”, and calls for improvements in fiscal transparency, notably by the adoption of the International Public Sector Accounting Standards (IPSAS). Government has in fact indicated to the IMF its intention to implement IPSAS by 2022/23.

Debt Sustainability

There are no conclusive grounds for determining a critical threshold of the country’s PSD, beyond which its credit rating is impaired and its financial stability endangered. Debt phobia is unwarranted when interest rates are low and debt is used productively to deliver faster growth. What is better known is that an elevated public debt ratio in an economy beset by a growing external imbalance, and by weakening growth, raises the risks of financial instability in the face of adverse local and external shocks. The likelihood of a financial meltdown is mitigated when debt is denominated mostly in local currency, of longer maturity and on more concessional terms.

An evaluation of debt sustainability for Mauritius would account for this complex and sometimes conflicting mix of factors. But it can be agreed, on a wide consensus, that incurring rising fiscal deficits on the strength of social spending rather than productive investments is not favourable to our long-term debt sustainability. Official statements that the latest IMF Report gives a clean chit to the country’s debt sustainability are grossly misleading. The IMF Report in fact expresses major concerns about the “elevated debt level”, and refers to “additional fiscal risks that require the debt level to be contained”.

It unequivocally states that “Fiscal adjustment is necessary to enhance fiscal credibility and preserve debt sustainability”, and recommends that Government should “pursue fiscal consolidation for the forthcoming budget FY2019/20 to build fiscal credibility and set public debt firmly on a declining path in the medium term”. Both revenue enhancing and expenditure reducing measures are recommended to contain the fiscal deficit and public debt. Government in its response concedes that fiscal correction is needed, and states in the IMF Report that “options to mobilize revenue and streamline expenditure to support consolidation are being explored.”

Financing Pressures

The resort to extreme measures to meet Government’s financing needs belies the notion that public debt is not an acute and burning issue. These exceptional budgetary measures include (i) raiding both the central bank’s capital reserves for Rs18 bn, and the surplus capital reserves of the Financial Services Commission for an estimated Rs0.6 bn, (ii) scraping the bottom of the barrel, with surplus cash balances of Rs1.4 bn from special funds and statutory bodies, (iii) selling off Government’s shares in certain state owned companies, for Rs 5bn this year, and Rs 6bn next year, and (iv) the recourse to private sector financing for important social infrastructure projects.

On this last point, Government had announced in last year’s budget a programme for the construction of 7,800 social housing units by the NHDC, costing Rs12.7bn, to be financed from external sources, possibly China. This programme has now been abandoned and will, in the forthcoming year, form part of projects to be implemented through private sector participation under the PPP/BOT framework. The critical need for social housing infrastructure will now be subject to even more uncertainty, as a consequence of budget financing pressures.

BOM Reserves Transfer

These excessive funding measures signal that Government is acting in desperation to shore up its coffers. First, the proposed amendment to the Bank of Mauritius Act to allow for the use of its capital reserves for fiscal purposes, i.e., for transfers to Government, is highly controversial. An indiscriminate opening of the floodgates for deficit financing can undermine the central bank’s independence and damage its credibility in financial markets.

The magnitude of the transfer, and the continuing significant losses incurred by the BOM arising from the cost of open market operations, raise grave concerns. Other related issues are raised in Box – Masters of Deception (1.3). It is crucial for the BOM to maintain an adequate level of capital reserves to safeguard against adverse risks, without compromising its ability to carry out its statutory objectives. Countries resort to such exceptional surplus transfers from the central bank only in emergency situations, and only to a limited extent. The India case may provide useful guidance on this contentious issue, outlined in Box 3: Transfer of Central Bank Surplus Reserves in India.

Box 3: Transfer of Central Bank Surplus Reserves in India

Last year, the Indian Finance Minister expressed the wish that the excess capital reserves of the Reserve Bank of India (RBI) should be transferred to Government. This was one of several issues that led the then RBI Governor, Urjit Patel, to resign in December 2018. In the same month, a 6-member expert committee was set up by the RBI, chaired by a former RBI Governor, to review the economic capital framework of the RBI.

The Committee’s mandate is to propose the adequate level of risk provisioning and profits distribution of the RBI, after reviewing the status, need and justification of RBI provisions, reserves, and buffers, in the light of best practices followed by central banks in making provisions for risks.

The Committee was to submit its report in April 2019, but was later allowed a three month extension. The Committee has so far failed to arrive at a consensus, and a last meeting is planned to finalise its report by the end of June 2019. It is reported that most members of the committee are favourable only to a phased transfer of the RBI’s excess capital reserves in order to keep a strong balance sheet to safeguard against a possible crisis and external shocks, whereas the Government representative on the committee is insisting on a one-time transfer.

The claim that the IMF recommends the use of reserves to meet our external objectives, including external debt repayment, is patently false when referring to capital reserves of the central bank. If a minister of finance cannot distinguish between a central bank’s capital reserves and its foreign exchange reserves, it may be time to close up shop and go fishing.

Before any legislative amendment to the BOM Act, it is strongly recommended that a study be conducted by the IMF on the appropriate economic capital framework for the BOM, to determine the level and adequacy of the BOM’s capital reserves, and review its surplus distribution policy.

Deficit Financing

The transfer of BOM reserves is for financing the Government budget deficit. There are two separate decisions underlying the use of BOM reserves to pay/prepay external debt, whereas Government is misleadingly presenting this as a single transaction, as if the BOM reserves will be used directly for repayment of external debt.

First, is the decision to transfer Rs18 bn to Government from the BOM, to be implemented after amendment of the BOM Act? Second, is a decision to pay/pre-pay external debt from Government funds, which is wise, as it would bring down the foreign currency share of public debt?

If the external debt repayment is financed by domestic borrowings, the total public debt would be unchanged. In the absence of exceptional windfalls like BOM reserve transfers or Govt equity sales, the only way to repay external debt and reduce total debt is to run a drastically lower fiscal deficit.

Thus, the BOM transfer of Rs18 bn, as well as Govt equity sales, provides Government with the means to finance a much higher fiscal deficit. The Government-inspired perception, reinforced by a BOM communiqué, that the central bank reserves transfer is of neutral consequences because of its use for external debt repayment is blatantly wrong. The use of BOM reserves by Govt, for whatever purpose, is first and foremost, central bank deficit financing.

Economic fundamentals

The international economic environment is currently characterized by considerable uncertainty. A lagging global economy and a slowing of trade and capital flows constitute potential downside risks for Mauritius, which is already grappling with a large external current account deficit and stagnant growth. Savings are dismally low, and the improvement in the investment rate remains modest. Public investments have recovered only from last year, and private investments are not expected to grow this year. Inflation remains subdued mainly on account of depressed prices of international prices of oil and commodities. Unemployment appears limited, although employment creation is poor and under-employment is significant.

The financial services sector, the topmost contributor to growth, is increasingly vulnerable to the implementation of fast-changing global tax and transparency standards. Manufacturing, Tourism, Sugar, and other export sectors are floundering. Any adverse shock leading to a sharp reduction in capital inflows would send the balance of payments into potential difficulties. Some ominous signs have begun to appear. The balance of payments surplus in 2018 was lower at Rs16 bn compared to Rs28 bn in the previous year. Exceptionally, successive balance of payments deficits were recorded in the last two quarters of 2018, and foreign exchange reserves declined from a peak of Rs230 bn in June 2018 to Rs217 bn in Dec 2018.

In response, the BOM has been feverishly accumulating foreign exchange as from early this year up to Rs239 bn in May 2019, to present an improved external reserves and balance of payments position for the current fiscal year. The widening external imbalance and the worsening of external competitiveness remain major sources of concern. In the event of a marked slowdown in capital inflows, sharp adjustments in the value of the rupee may become inevitable.

Conclusion

Key economic fundamentals are on a weakening trend, and the pursuit of spendthrift fiscal policies in such a context is ill-conceived and irresponsible. Fiscal deficits are too high, and public debt is being pushed to unsustainable levels. The IMF is urging for immediate fiscal adjustments to enhance fiscal credibility, preserve debt sustainability, and to help in containing the external current account deficit.

The expansion and modernization of capital infrastructure has paid the price for the disproportionate focus on social spending. The recourse to extreme financing such as the BOM reserves transfer, or the sale of Government assets, are only stop-gap measures to elude the need to reduce an oversize fiscal deficit. The BOM Act should not be amended prior to a review, preferably by the IMF, of the BOM’s economic capital framework. The integrity of fiscal statistics should not be compromised by doubtful practices, and IPSAS should be implemented as early as possible.

Finally, it remains a priority to strengthen public investment management, and to reintroduce programme-based budgeting (PBB), albeit in revised form, to ensure a cost-effective management of public investments. Quoting from a 2010 PBB Manual of the Ministry of Finance, countries introducing PBB “have typically been concerned about a high level of public debt and excessive budget deficits …”

Masters of Deception

1.1. – Budget Deficit

Governments across the world allow for some degree of dressing-up of their accounts to present fiscal outcomes in a better light. In Mauritius, the erroneous and contrived accounting practices adopted by successive Governments have raised the art of fiscal deception to new heights.

To underestimate the true size of the fiscal deficit, a standard practice has been to redirect Government expenditures to off-budget public vehicles, such as the National Infrastructure Development Fund, the Privatization Fund, and Special Funds. More recently, the creation of Special Purpose Vehicles such as Metro Express, and Multi Sports Infrastructure, has served this purpose, since Government contributions to these vehicles have been framed as equity injections and not expenditures. Foreign lines of credit are also made to bypass Government to finance expenditures in Metro Express, Mauritius Telecom and other public entities.

In recent years, substantial unspent balances in special funds have also been transferred back to Government, and wrongly classified as revenue to artificially improve the fiscal deficit. The consolidation of special funds with the budget, as done by the IMF in its country reports on Mauritius, is a necessary correction, to account for off budget expenditures and to adjust for actual revenue. The actual fiscal deficit must account for all off-budget expenditures by public entities. Probably under pressure from the IMF, the Government Estimates, 2019/20 now provide on the last page (Appendix H, Table H4) details of off-budget expenditures by 4 public entities.

The accounting of State Trading Corporation (STC) operations is not directed at manipulating the fiscal deficit, but to hide the true extent of commodity subsidies in Government accounts. Petroleum tax revenues are deflected to the STC instead of being credited to Government revenue, and are used partly for commodity subsidization. Only the net surplus of STC revenue is credited to Government. A proper consolidation of Government and STC operations is required for a proper analysis of Government subsidies and expenditures.

Another improper accounting treatment is the inclusion in Government revenue in 2019/20 of a sum of Rs1.4 bn representing a transfer of surplus cash balances from miscellaneous statutory bodies and special funds, in order to curtail the budget deficit. The use of surplus cash balances is a financing item for the budget, not a revenue item. Through a consolidation with Government operations, such transfers must be excluded from revenue.

1.2. – Public Debt

The public sector debt (PSD) is equally the target of duplicitous efforts at underestimation, especially in view of the need to comply with the statutory ceilings under the Public Debt Management Act. In Dec 2018, PSD was reduced by Rs2.9 bn, or by a “Consolidation adjustment in respect of Govt securities held by non-financial public corporations”.

This adjustment item results from an exercise to consolidate Government with non-financial public enterprises, and to exclude Government securities held by these enterprises from public debt. The computation of PSD was until Dec 2018 done on an aggregated basis, but was modified in Dec 2018 to a consolidation basis only to prevent PSD from exceeding the ceiling of 65% of GDP.

However, this consolidation exercise is arbitrarily selective. For instance, social security funds should also be consolidated, which would similarly exclude Govt securities held by the NPF from PSD, but would also raise PSD by the amount of the NPF’s liabilities. Liabilities of non-financial public enterprises, such as accounts payable, should also be added to PSD upon consolidation.

The consolidation adjustment item is a crooked device to underestimate public debt. It was also used to reduce PSD by a higher amount, or Rs4.5 bn, in March 2019. Although this adjustment item is officially estimated at Rs4 bn in June 2019, it is likely to be boosted further by the new issue of Government Treasury Certificates for Non-Financial Public Sector Bodies (NFPSB). This BOM-conducted issue, aimed specifically and directly at NFPSB, and by-passing primary dealers, is perceived as a convoluted scheme to artificially bring down the value of PSD.

External lines of Credit, namely of India Eximbank to SBM for the Metro Express and China Eximbank to Mauritius Telecom for the Safe City Project, are now included in PSD, but only to the extent that credits are disbursed. For greater fiscal transparency, PSD should also be calculated to reflect debt commitments and not only debt disbursements.

1.3. – BOM reserves transfer

A final example of manipulation of budgetary accounts relates to the treatment of the transfer of Rs18 bn to Government from the capital reserves of the Bank of Mauritius in 2019/20. While this BOM transfer cannot be considered as Government revenue because it originates from its capital reserves and not its profits, it is a financing item for the budget and should be classified accordingly. But, in order to conceal the connection between the budget deficit and its financing by the BOM, the amount of Rs18 bn is misleadingly incorporated in a separate table on the Government Financing Plan, for financing repayment/early repayment of external debt.

Under IMF fiscal accounting standards, the 2019/20 Budget Estimates should have recorded this reserves transfer from the BOM in its Statement of Government Operations under “Net Acquisition of Financial Assets”, as a positive financing item representing “Proceeds from Government Equity Participation in BOM”, along with equity sales or loan reimbursements. It would thus be clear that the BOM transfer proceeds of Rs18bn are a financing item for the 2019/20 budget deficit.

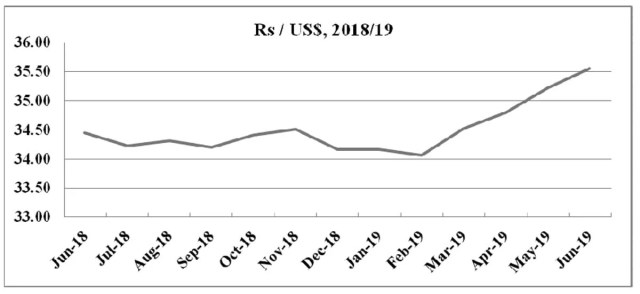

The BOM has been intervening aggressively on foreign exchange markets to depreciate the rupee since March 2019, putting pressure on banks to align their rate quotations to BOM pre-determined rates. As shown in the attached chart, the US Dollar shows an appreciation of over 3% against the rupee between June 2018 and June 2019.

Recent BOM intervention helped generate an additional Rs7bn of valuation gains on the current level of over Rs230 bn of foreign exchange reserves. The BOM Special Reserve Fund, which stood at Rs13 bn in June 2018, was thus boosted to Rs20 bn at June 2019. Financial markets are already apprehensive of this flagrant exchange rate manipulation to engineer a transfer of Rs18 bn from the BOM Special Reserve Fund.

* Published in print edition on 19 June 2019

An Appeal

Dear Reader

65 years ago Mauritius Times was founded with a resolve to fight for justice and fairness and the advancement of the public good. It has never deviated from this principle no matter how daunting the challenges and how costly the price it has had to pay at different times of our history.

With print journalism struggling to keep afloat due to falling advertising revenues and the wide availability of free sources of information, it is crucially important for the Mauritius Times to survive and prosper. We can only continue doing it with the support of our readers.

The best way you can support our efforts is to take a subscription or by making a recurring donation through a Standing Order to our non-profit Foundation.

Thank you.